Europe is trying to reduce its heavy dependence on American payment companies such as Visa, Mastercard, PayPal, and Apple, but growing disagreements between policymakers and financial institutions are slowing down the process.

As digital payments become a normal part of everyday life, European authorities are becoming increasingly concerned about how much of the continent’s financial activity relies on foreign technology and payment systems. The issue has gained urgency in recent years as cashless payments have surged following the COVID-19 pandemic, changing the way millions of people shop, bank, and transfer money.

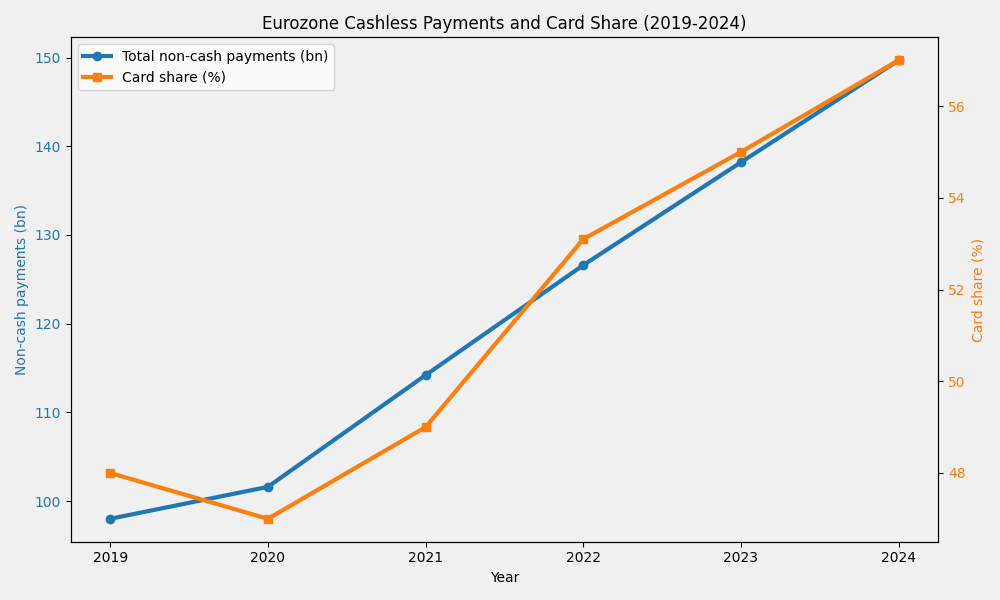

Today, companies like Visa and Mastercard process nearly two-thirds of card payments across the eurozone, making them deeply embedded in Europe’s financial ecosystem. While these platforms have helped make payments faster and more convenient, European policymakers worry that depending too heavily on non-European firms creates financial and strategic vulnerabilities.

In simple terms, Europe wants greater control over how money moves within its own borders and hopes to create a stronger, homegrown payment system that can compete with global players.

At the center of this effort is the European Central Bank’s push for a digital euro, a state-backed digital currency designed to make electronic payments easier, safer, and more independent from foreign payment systems. The idea is part of a broader strategy to strengthen Europe’s payment sovereignty, a term used to describe a country or region having greater control over its financial infrastructure rather than relying on outside companies.

See Related: Strategy Slashes 2029 Debt With $1.5B Convertible Buyback

However, Europe’s ambitions have created tensions between regulators and banks. While both sides agree on the long-term goal of modernizing payments and reducing dependence on foreign systems, disagreements have emerged over costs, timelines, and business incentives. Banks and payment firms fear that the proposed system could reduce their revenues, especially if new rules place limits on the fees merchants pay for digital transactions.

The European Central Bank plans to provide digital euro infrastructure free of charge and cap merchant fees, a move designed to encourage widespread adoption but one that could significantly reduce income for private payment companies.

Financial Stakes And Card Payments

The financial stakes are enormous. Card payments in the eurozone are worth roughly €3.4 trillion annually, meaning even small changes in fees could have a major financial impact. Estimates suggest the private payments industry could lose between €8 billion and €9 billion in annual revenue if merchant fees are restricted under the proposed system.

This concern has contributed to delays in legislation surrounding the digital euro, with discussions in the European Parliament dragging on for nearly three years as policymakers and financial institutions continue to debate how the system should function.

At the same time, private sector initiatives are beginning to emerge alongside public efforts. Recently, 25 additional banks, including major institutions from across Europe, joined a consortium working on a euro-pegged cryptocurrency, highlighting how banks are also exploring digital alternatives to traditional payment systems.

While these efforts move in a similar direction to the European Central Bank’s plans, experts say the biggest challenge lies in aligning public policy goals with private business interests.

The real question facing Europe is whether it can create a payment system that gives consumers more choice, strengthens financial independence, and lowers costs without hurting innovation or reducing incentives for banks and payment providers.

Striking that balance will determine whether Europe succeeds in reshaping its digital payments future or continues relying heavily on U.S. financial technology giants.

As digital transactions continue to replace cash, the debate is becoming more important than ever. Europe’s attempt to build payment independence is not just about technology or banking profits; it is about economic control, financial security, and deciding who shapes the future of money in an increasingly digital world.